.avif)

%20(1).avif)

Key Takeaways

- While lessors were not hit as directly by the new lease accounting standards, the aftermath of ASC 842 will inevitably affect the accounting policies and practices of both parties to any lease agreement. However, the basics of lessor accounting have not really changed under the ASC 842 standards.

- For both sales-type and direct financing leases, an amortization schedule can be generated to easily capture the lessor journal entries for each month of the lease term.

- While the journal entries for sales-type and direct financing are generally the same, differences do arise in how they record any associated selling profit. NetLessor can help you meet the demands of lessor lease accounting

There is no question that the new leasing standards under ASC 842 have drastically changed the accounting game. With bright-line tests being replaced for more in-depth analyses, lessees everywhere are frantically trying to determine how to properly classify and book their leases between the operating and finance categories under the new ruleset.

Just as it takes two to tango, it also takes two to enter lease agreements. Thus, an important question arises: Do the new standards affect the way lessors book their lease transactions?

While there are changes between ASC 840 and ASC 842 that will inevitably impact the lessor, the (beautiful) truth of the matter is that the basics of lessor accounting have not really changed under the new standards.

In this article, I hope to provide a quick reminder of the fundamental journal entries and financial statement impacts a lessor can expect when dealing with two of the three major lease class-types of lessor accounting (sales-type and direct financing). More specifically, in the downloadable tool and for the remainder of this article, I will touch on the following:

- How to determine the classification a lessor should use for a lease—see Procedure 1 in the downloadable file, which includes a tool to help in determining lease classification.

- Example amortization schedules for both sales-type and direct financing leases—see below and Procedures 2-3 in the downloadable file.

- Example journal entries that would be booked for each lease classification—see below and Procedures 2-3 in the downloadable file.

- The income statement and balance sheet impact of each classification. See below and Procedure 4 of the downloadable file.

Amortization Schedules

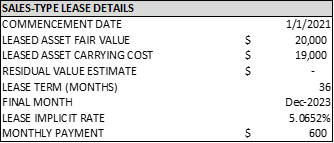

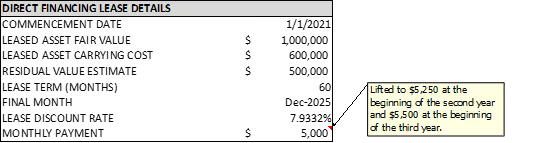

For both sales-type and direct financing leases, an amortization schedule can be generated to easily capture the lessor journal entries for each month of the lease term. See Procedures 2-3 in the downloadable file for examples of these amortization schedules. The amortization schedules and images through the remainder of this article are based on the following lease details for an example sales-type lease and an example direct financing lease respectively:

Journal Entries

While the journal entries for sales-type and direct financing are very similar, differences do arise in how they record any associated selling profit.

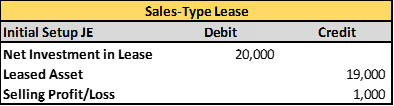

Sales-Type Leases

When a lease meets the criteria to be classified as a sales-type lease, the idea is that the lease should be treated as if it was… well… sold. Therefore, the underlying asset should be taken off the books and the net investment in the lease should be recorded. In addition, the income statement could also be impacted as any sales profit or loss resulting from the transaction will need to be recorded at the time that the lease commences.

- Credit: Leased Asset—remove the carrying cost of the asset

- Debit: Net Investment in Lease—equivalent to the present value of any lease payments plus any underlying residual value

- Credit/Debit: Selling Profit/Loss—recognize any profit/loss on the commencement date

After booking the initial balance entry, the lessor will have periodic amortization entries that will be recorded over the life of the lease. Within these entries, the lessor will recognize any associated interest income based on the effective rate of interest, and in turn the net investment in the lease will be adjusted in accordance with the amounts of the interest income and the related payment.

- Debit: Lease Receivable (or Cash)—represents the lease payment required for the period

- Credit: Interest Revenue—interest for the period calculated by multiplying the running lease balance by the implicit rate1 in the lease.

- Credit: Net Investment in Lease—increased by any interest revenue and decreased by any required lease payment

1US GAAP 842-30-20 Rate Implicit in the Lease. The rate of interest that, at a given date, causes the aggregate present value of (a) the lease payments and (b) the amount that a lessor expects to derive from the underlying asset following the end of the lease term to equal the sum of (1) the fair value of the underlying asset minus any related investment tax credit retained and expected to be realized by the lessor and (2) any deferred initial direct costs of the lessor. However, if the rate determined in accordance with the preceding sentence is less than zero, a rate implicit in the lease of zero shall be used.

Direct Financing Leases

For any leases that meet the specifications to be classified as a direct financing lease, the bulk of the accounting treatment is similar to how we record their sales-type cousins. Essentially, the lessor will still need to derecognize the underlying asset and record an investment in the lease. Unlike sales-type leases, however, any sales profit associated with the lease will be deferred and not recognized on the date of the lease commencement. Note that this is only in the case of there being selling profit, as any loss would still be recognized on the commencement date for a direct financing lease.

Moreover, the lessor will also generate amortization journal entries over the life of the lease—increasing the net investment in the lease for any interest income recognized and decreasing the net investment for any payments. Another important difference between the two lease types arises in the calculation of the interest revenue for these amortization entries, as direct financing leases utilize the lease discount rate2 and not the implicit rate calculated for sales-type leases.

2This is the rate of interest that, at a given date, causes the aggregate present value of (a) the lease payments and (b) the amount that a lessor expects to derive from the underlying asset following the end of the lease term to equal the sum of (1) the CARRYING COST of the underlying asset minus any related investment tax credit retained and expected to be realized by the lessor and (2) any deferred initial direct costs of the lessor.

Financial Statement Impact

Income Statement

For both sales-type and direct financing leases, interest revenue will need to be reported on the income statement. As noted above, however, sales-type interest amounts are based on the implicit interest rate in the lease, while direct financing utilizes the lease discount rate.

In addition, the income statement will also be impacted for sales-type leases in that any selling profit or loss is required to be recognized as of the lease commencement date. Meanwhile, the rules for direct financing leases dictate that only a selling loss would need to be recognized on the commencement date—as any selling profit would be deferred.

Balance Sheet

A lessor’s balance sheet will be affected by both sales-type and direct financing leases in a similar manner. Cash or receivable accounts will be increased based on the associated lease payments, and the net investment in the lease—which should be reported distinctly from other assets on the balance sheet—will be adjusted according to the lease activity for the period.

Bottom Line

While lessors were not hit as directly by the new lease accounting standards, the aftermath of ASC 842 will inevitably affect the accounting policies and practices of both parties to any lease agreement. Now more than ever it is important for lessors to understand the proper way to book and report their leases. A great first step in this endeavor is to have a grasp on the fundamental journal entries associated with sales-type and direct financing leases.

Even with a strong comprehension of lease-accounting expectations, keeping track of all your leases can be a sticky, arduous, and time-consuming practice. If you are finding yourself bogged down with meeting the demands of lessor lease accounting, an automated software solution like NetLessor could be an invaluable investment for your business.