When a company enters into a real estate lease, they often make changes to the property to make it fit for their operations.

Both the lessor and lessee can make these lease improvements, helping ensure the property is useful for the lessee.

We see leasehold improvements every day in the leasing world, but how do companies account for them, and how has ASC 842 changed the process?

This blog post will cover everything you need to know about accounting for leasehold improvements under ASC 842.

What are leasehold improvements?

Leasehold improvements are changes made to a property when a company enters into a real estate lease. These changes are accounted for as fixed assets. Lease improvements help ensure the property will meet the lessee’s needs, and they can be made by the landlord (lessor) or the tenant (lessee).

Examples of common leasehold improvements include:

- Replacing the flooring, carpet, or tiling

- Changing the light fixtures

- Building or removing walls

- Adding cubicles

- Adding retail shelving

- Installing or updating plumbing

The lessor might sweeten the lease deal by offering to pay for certain leasehold improvements that the lessee needs. They might even offer special buildouts to entice the company to renew the lease or extend the term.

These incentives to lease the property are called lease incentives and need to be accounted for as a part of the lease agreement. Next, we’ll explore how that works.

How do tenant improvements and lease incentives work?

Lessors often provide lease incentives by offering a tenant improvement allowance. This allowance gives the tenant a certain dollar amount to perform and manage leasehold improvements.

The tenant improvement allowance is either paid to a third party on behalf of the lessee or as a reimbursement directly to the lessee. The lessor can provide the allowance in cash before lease commencement or anytime during the term of the lease contract.

A tenant improvement allowance is recognized as a lease incentive. As the guidance states under ASC 842-10-55-30, lease incentives include:

- Payments made to or on behalf of the lessee

- Losses incurred by the lessor as a result of assuming a lessee’s preexisting lease with a third party

How leasehold improvements worked under ASC 840

ASC 840, the previous lease accounting standard, required tenant improvements (lease incentives) to be reflected as a reduction to the minimum payments. Therefore, the lessee would record an asset for the improvement, and the incentive/reimbursement was recorded as a deferred rent credit.

The deferred rent credit was then amortized as a reduction to rent expense.

Let’s see it in action for a lease with the following details:

- Term: 24 months

- Monthly payment: $1,000

- Lease incentive: $2,000

The initial balance entry would look like this:

And the monthly amortization entries would look like this:

How accounting for leasehold improvements works under ASC 842

Under ASC 842, the current lease accounting standard, tenant improvements (lease incentives) must be recorded as a reduction of fixed payments. This will, in turn, reduce the right-of-use (ROU) asset from the time it is capitalized at lease commencement.

Similar to ASC 840, the lessee will record an asset for the improvement. But instead of recording a deferred rent credit, they will reduce the ROU asset by the same amount. The reduction in rent expense will be carried through to the amortization of the ROU asset.

Let’s see what it looks like for the same lease as above, this time under ASC 842:

- Term: 24 months

- Monthly payment: $1,000

- Lease incentive: $2,000

The initial balance entry would look like this:

And the monthly amortizations entries would look like this:

If the lease incentive is scheduled to happen at a certain point in the lease, it should be included in that period's lease payment as a reduction and discounted back to the lease commencement date and recorded at its present value.

When the timing of the lease incentive is uncertain, the accounting can become a little trickier. For further guidance, refer to Lease incentives: What to do when timing is uncertain.

Learn more about leasehold improvements

Find answers to common questions about leasehold improvements below.

Is a tenant improvement allowance considered income?

No, a tenant improvement allowance is not considered income. The allowance is typically negotiated as part of the lease agreement between the landlord and the tenant, and it can be used to cover the cost of construction, renovation, or other improvements to the leased space that are required by the tenant.

The amount of the allowance provided by the landlord can vary, and it may be provided as a lump sum or as a reimbursement for specific expenses.

It's important to note that while the allowance is not considered income, it may have tax implications for the tenant. Depending on the specific circumstances, the use of allowance funds may be subject to certain tax rules and regulations, so it's always a good idea to consult with a tax professional for advice.

Are tenant improvements amortized?

Yes, tenant improvements are typically amortized over the life of the lease. Amortization is an accounting technique that reduces the book value of a loan or intangible asset over a specified period. Typically, the amortization is repaid in installments over the lease term, with interest.

Leasehold improvements can be quite costly, and it may not make sense for a landlord to expense the entire cost in the year the improvement is made. Instead, the landlord can choose to amortize the cost of the tenant improvements over the expected useful life of the improvement.

The amortization period for tenant improvements will depend on various factors, such as the nature of the improvement, its expected useful life, and any applicable tax regulations.

Should tenant improvements be capitalized?

Yes, tenant improvements should be capitalized as they are long-term assets that add value to a property. Tenant improvements that extend the useful life of the property, enhance the property's value or functionality, and increase the property's capacity or productivity should be capitalized.

Capitalizing the cost of tenant improvements means that the cost is recorded as an asset on the balance sheet and is depreciated over the useful life of the improvement.

Is a tenant improvement an expense?

Yes, a tenant improvement is an expense incurred to alter or remodel a rental property to make it suitable for a tenant. This can include painting, replacing carpets, installing new fixtures, and more.

However, from an accounting perspective, tenant improvements can be treated as either an expense or a capital expenditure, depending on the nature and cost of the improvements.

If the improvements are considered routine maintenance or repairs, they are typically expensed as incurred. However, if the improvements are significant and increase the value of the property, they may be capitalized and depreciated over time.

Simplify lease accounting with NetLease

Ensuring all aspects of your leases comply with ASC 842 is vital, but it doesn’t have to be complicated.

The right lease accounting software can simplify the process with automated schedule generation and guaranteed compliance with accounting standards.

NetLease makes the process of adding tenant improvement allowances to your lease schedule simple, whether those incentives are given before lease commencement or during the term of the lease.

If the allowance is given before lease commencement, NetLease allows you to input the amount in a Lease Incentive field. NetLease will automatically apply that amount to the appropriate sections within the schedule.

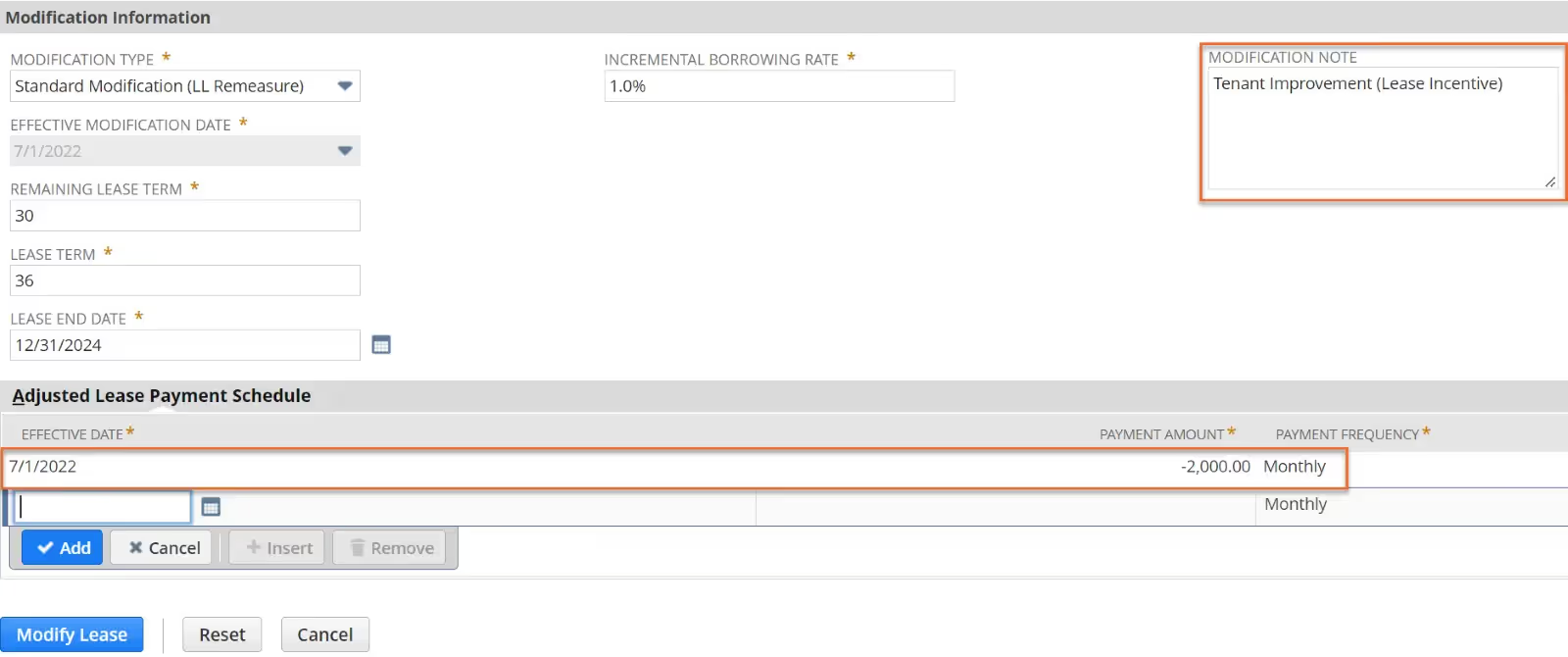

When a tenant improvement is given during the term of the lease, NetLease allows for a lease modification, where the amount can be used to adjust the payment in the period it is received. NetLease will then adjust the lease schedule based on the new information.

This is just one of the ways in which Netgain’s lease accounting solutions simplify the complexities of lease accounting for lessors and lessees—whether you use NetLease or another enterprise resource planning platform.

Take a self-guided tour of our solutions or request a personalized demo to discover how you can achieve compliance and reclaim time by streamlining tedious tasks.